As early-stage tech, startups and entrepreneurism go mainstream, more investors are willing to invest in VC.

With some of the highest potential returns among asset classes, venture capital (VC) is increasingly attracting investors. VC as an asset class has its own characteristics and it may be a good addition to complement any given investor’s portfolio

Tech and VC

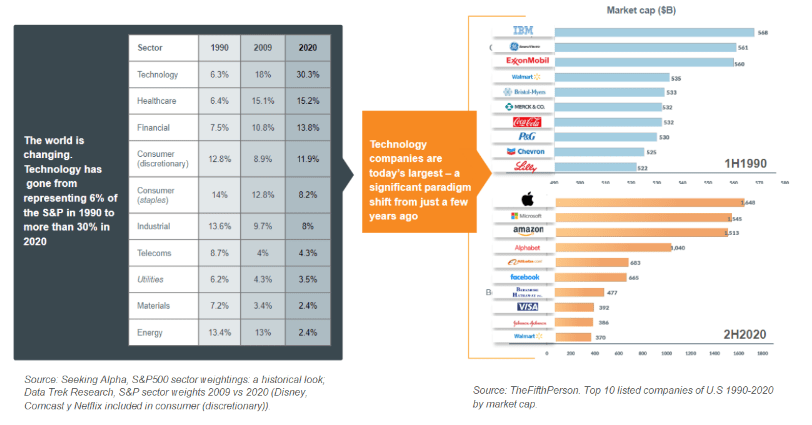

The world is evolving and, to a significant extent, is doing so driven by technological progress. The global tech leaders – including the likes of Amazon, Google, Apple, Microsoft… and many more – were once small projects that started up in their founders’ garages or in university rooms, which progressively grew thanks to the support of private capital.

In a nutshell, VC is the private capital used to support technology-based companies in their early stages (i.e startups and scale-ups). From its origins in the 1970s in California’s Silicon Valley all the way through today, VC has become an asset class with its own identity within the private capital universe. Moreover, VC has, for many years now, transcended American borders to become a driving force behind technological innovation on a global scale.

VC as an asset class

VC is a part of a large asset class commonly referred to as private capital, which encompasses other subclasses such as private equity, infrastructure, etc. VC shares some characteristics with these “sister” subclasses but has others unique to it. Thus, anyone considering investing in VC should necessarily take into account and understand the following characteristics:

Long-term: VC investments have long maturity horizons of at least eight-to-ten years, as the target is early-stage companies that need time to scale, mature, and eventually be exited/divested (usually through M&A transactions or IPOs). Such long terms also mean that VC is less exposed to short-term market fluctuations.

Illiquidity: VC is an illiquid asset, in the sense that once the investment has been made, there are – as a general rule – limitations in place for the investor to cash out before the underlying companies are exited.

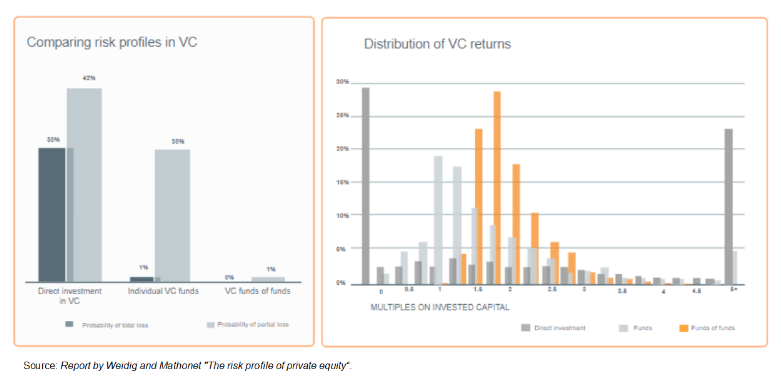

High potential returns: VC is a high-risk asset. It invests in young companies with high levels of uncertainty, meaning many will not prosper. But at the same time, it can generate extraordinary returns when the invested startups do very well. Therefore, it is critical to invest in VC systematically and with a diversified approach.

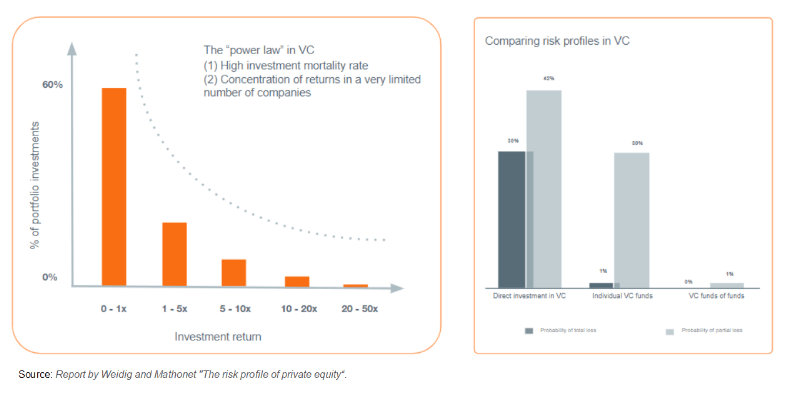

Access to the best startups is not an easy task, and there is significant competition. In other words, the best opportunities are typically not available to the generality of investors. Hence, regardless of the investment means (i.e. directly into startups, VC funds, funds of VC funds), it is critical for anyone looking to invest in VC to do so through those who enjoy such access and have a thorough knowledge of the market.

Singular distribution of returns: VC funds returns do not follow a normal distribution, but a “power-law” curve, which means that returns tend to be concentrated in a small percentage of companies. A tiny number of startup investments will be fund-returners and generate very high returns, while most of the other portfolio companies will die or just make back the investment.

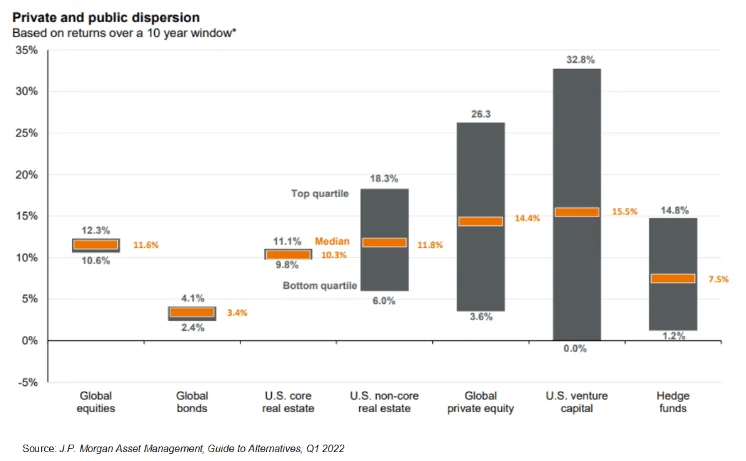

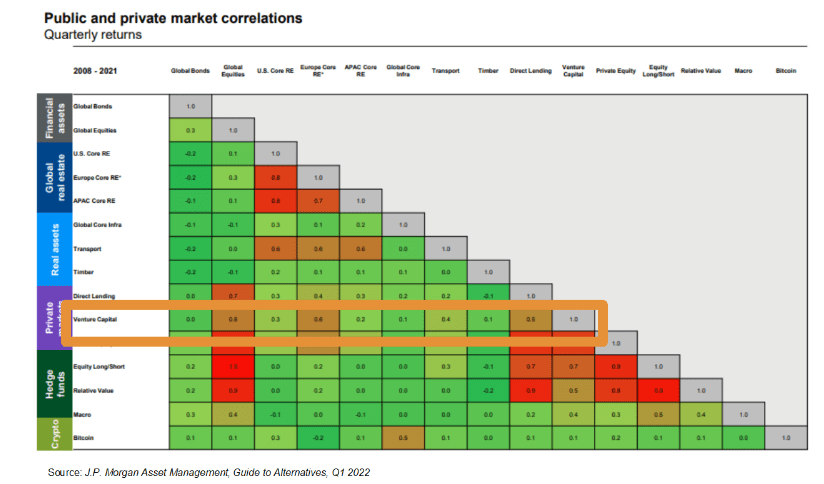

Uncorrelation: VC is an asset with a low correlation with other asset classes, making it attractive to construct diversified investment portfolios.

Public and private market correlations

Quarterlay returns

The opportunity in Europe

Historically, it has been typical to identify tech, startups, and VCs in the US, in particular with Silicon Valley. But that is no longer the case. Leaving Asia aside (where the activity is significant, in particular in China), over the last two decades, the European tech ecosystem has developed very significantly and it is expected that it will continue doing so.

Strongly supported by the European governments and institutions, the maturity of the European tech ecosystem is evident at all levels. This has materialized in different ways, such as the increasing number and quality of entrepreneurial projects, the setting up of more qualified VC managers, institutional and non- institutional capital more willing to invest in VCs, proven success stories (300+ European “unicorn” companies now valued at more than €1B and hundreds of “soonicorns”), a more dynamic exit (M&A, IPOs) playing field and an increasingly favorable regulatory environment. We in Europe are on the right path.

Contrary to what one might think, European VC has demonstrated its ability to generate higher returns than American VC on a sustained basis over time. Due to the oldest development of the US ecosystem, startup valuations in Europe are still a fraction of their American counterparts across all stages. Being able to invest more cheaply and take advantage of a multiple exit arbitrage seems, at first sight, a no-brainer. And the fact that Europe has demonstrated that it can produce global leaders reinforces that idea.

Conclusion

There is no doubt that we are witnessing a technology boom financed by VC. The weight of technology in the world continues to increase, and the development we have been observing in the global and European tech ecosystem bears witness to this.

Even in this favorable environment, VC is still a relatively unknown asset class for many investors, both large and small. It is a fact that the interest in VC investing is growing in Europe in parallel with the ecosystem development and the multiple success stories that are giving rise to international champions which, in turn, are proving VC’s capacity to generate extraordinary returns and to help diversify any investment portfolio.

As the complex asset it is, any investor interested in investing in VC must do so systematically, fully understanding its characteristics and ensuring a weight in her portfolio that fits her risk profile.

ARTICLE AUTHOR

Diego Recondo

Co-Managing Partner at All Iron Ventures

Diego is a partner and co-managing director of All Iron Ventures, a VC firm based in Bilbao, Spain, with ~€110M AUM. Further to his involvement in the firm’s investment committee, Diego is in charge of day-to-day operations (investor relations, legal, structuring, platform, marketing). In 2020 AIV closed what is to date the largest debut VC fund ever raised in Spain. Previously, Diego worked for 15+ years as a business development executive in both traditional and startup environments, and also as an M&A lawyer and angel investor.